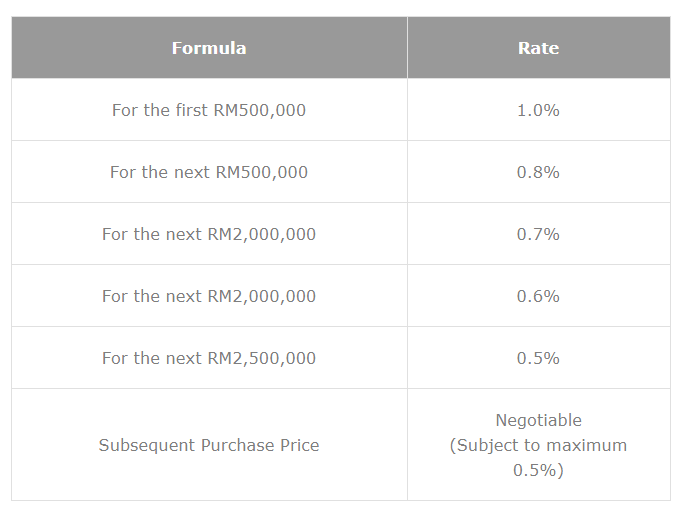

Essential insights on stamp duty in Malaysia for buying commercial and industrial properties, covering taxes and exemptions.

KIMBERLY OOI

BUSINESS MANGER PENANG AREA

MALAYSIA‘S REGISTERED SENIOR INDUSTRIAL REAL ESTATE NEGOTIATOR VERIFIED AGENT IN IPROPERTY ...